National Portal Of India

National Portal Of India

Weaving the Way for Indian Textile Industry

The textile and apparel industry is one of the earliest industries to have developed in India. Its inherent and unique strength is its incomparable employment potential owing to the presence of the entire value chain from fibre to apparel manufacturing within the country. It is the biggest employer after agriculture and provides direct employment to 4.5 crore people and another 6 crores in allied sectors. India needs to generate jobs that pay well, provide social protection to workers, support efficient production for export markets, and hold the potential for social transformation. The textile industry meets all these criteria.

India is the second-largest manufacturer of textiles and clothing in the world. India is also the second-largest exporter of textiles and apparel with a share of 5% of global trade. Exports of textile and clothing products, including handicrafts, from India have slightly increased to US$ 40.4 billion during the year 2018–19 from US$ 39.2 billion during 2017–18, registering a growth of 3%. However, India’s global share is way behind that of China, which has approximately 38% of the global textile and clothing trade. The share of textile and clothing in India’s total exports stood at 12% in 2018–19. With 48% total textile and apparel export, EU-28 and the United States are India’s major textile and apparel export destinations.

Overview of Textile Value Chain

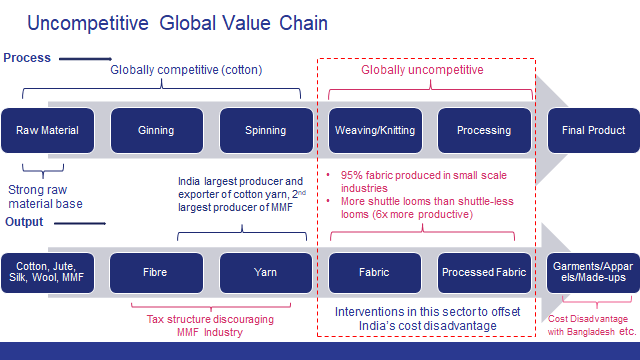

While India has the advantage of the entire value chain in the industry, currently the value chain is uncompetitive. The figure below indicates the current status of textile value chain (GVC) in India:

India has a very strong raw material base both in natural and manmade fibres (MMFs). India has emerged as the largest producer of cotton in the world with a production of 370 lakh bales in 2017–18 and the second-largest exporter of cotton. However, high contamination level and poor quality of fibre, both in fineness and length, are major concerns that need focused attention.

India has a strong presence in global exports of cotton yarn. Vietnam has increased its global export share of cotton yarn from 5% in 2012 to 15% in 2016. China and Bangladesh are the largest importers of cotton yarn from India, who in turn creates value addition to the yarn and then exports the same at a lower cost compared to India. India needs to upgrade its position from a supplier of cotton yarn to a producer of value-added fabrics and garments. As the world export value of cotton yarn has decreased over the years, it is an indication that the cotton textile trade is shifting towards different types of fibre such as MMF.

While India leads in cotton yarn exports, it has been a very marginal player when it comes to cotton fabric in world exports. China has a substantial share of 51% in cotton fabrics when compared to India’s 5%–6%; the situation is almost the same in case of MMF fabrics. This comparison suggests that India is not able to scale up the value chain significantly enough to meet the global demand despite being the largest producer and exporter of cotton yarn.

Approximately 95% of the weaving sector in India is unorganized in nature. The decentralized power loom and hosiery sector contributes 85% of total fabric production. The processing segment is also dominated by a large number of independent, small-scale enterprises. Since, the weaving/processing sector in India is dominated by small-scale enterprises, it has challenges such as inadequate know-how, low focus on research, innovation in new product development and low technology upgradation. Further, low productivity and automation levels also remain one of the biggest woes for the weaving industry. Due to these factors, the overall performance of fabric production in India is getting dampened. The weaving sector still remains one of the weakest links of the Indian textile and apparel industry.

India has one of the largest installed production bases in the world in weaving sector but at the same time it uses old technology with low productivity and quality levels. In terms of technology adoption in the weaving sector, India has only 2% share in global shuttle-less looms (i.e. modern looms) installed capacity. The cost of production in India also goes up due to poor technology levels and low scale of operations, as 95% of the weaving sector in India is unorganized and in small scale. India also lacks the presence of large fabric manufacturers when compared to China and the US.

Recommendations

In order to make the textile industry competitive, industry needs to focus on investing in technology upgradation and expand weaving capacity to scale-up operations. To ensure rapid transformation of the weaving sector in India, under Amended Technology Upgradation Funds Scheme (ATUFS) of the Government of India, the weaving sector may be considered to get capital subsidy at par with garmenting and technical textiles. At present, the weaving sector is getting subsidy at 10% subject to cap of 20 crore under ATUFS, whereas for garmenting and technical textiles, subsidy is provided at 15% subject to cap of 30 crore. For creating few global champions in weaving sector in India, the Government of India may consider providing some enhanced subsidy under ATUFS, for select players, purely on outcome basis. Further, state governments should aggressively promote infrastructure and provide plug and play parks for the industry. Lands should be allotted in such parks for long-term lease. The supply of uninterrupted quality power at fixed price for a tenure of 15 years may also be considered in these parks. To ensure rapid scaling up of business, state governments should provide all the approvals in place, including the provision of CETPs/ZLD, as per need basis, in these parks.

The weaving sector is the backbone of the textile industry. On the one hand, promoting the weaving industry gives impetus to the domestic spinning industry and on the other, it makes our garment’ sector globally more competitive. With focused interventions in this sector, we might enhance its performance in terms of more investment, employment generation and export earnings.

*Upendra Kumar Gupta is Deputy Adviser, NITI Aayog. Views expressed are personal.